The price of high-quality development

The most striking feature of current economic operation is that the speed of supply repair is obviously slower than that of demand improvement, and supply constraints have a negative impact on price stability and demand release. However, some of the supply constraints are aimed at reducing pollution, reducing debt and optimizing economic structure, which is the price that must be paid actively for high-quality development; The other part of the supply constraint is caused by the impact of global commodity production and industrial chain supply chain, which is also an acceptable reality for high-quality development. Looking forward to 2022, the expansion rate of total demand will further slow down, but the supply-side constraints may persist, and the "rebalancing" of the supply-demand gap still faces multiple obstacles.

1. Domestic economic forecast and suggestions on asset allocation

Judging from the actual economic situation, the economic situation in 2022 will be weaker than that in 2021.According to the follow-up, the improvement of consumption is limited, the bottoming role of real estate investment declines, the pulling role of exports weakens, the traditional infrastructure investment continues to fluctuate at a low level, and the rebound of manufacturing investment and new infrastructure is also difficult to support the total demand. Therefore, in 2022, the domestic economy will return to the long-term growth center.

We forecast the GDP growth rate of each quarter and the whole year in 2022 through the ring-on-ring growth rate under different assumptions.Under the neutral hypothesis, the year-on-year growth rate of GDP in the first four quarters of 2022 was 2.9%, 3.2%, 6.1% and 5.2%, and the annual GDP increased by 4.4%. The annual GDP increased by 3.5% under pessimistic circumstances and by 4.8% under optimistic circumstances. In all cases, the third quarter is the year-on-year economic high, but the base fluctuation caused by the COVID-19 epidemic will continue to affect the year-on-year trend of economic indicators in 2022. The year-on-year growth rate in the second half of the year is faster than that in the first half of the year.

How to accurately measure the trend of the year-on-year data of the real economy next year is a key issue to guide market investment.However, the two-year average growth is no longer applicable in 2022, because the two-year average growth is also affected by the base. According to the neutral scenario of GDP growth rate in 2022, the average growth rate in the first four quarters is 10.3%, 5.5%, 5.5% and 4.5% respectively, and the trend is exactly the same as that in 2021, which is of little significance for investment guidance. So, what indicators can be used to describe the economic rhythm in 2022 more accurately?

Starting from the idea of cross-cycle adjustment, we can consider the average growth for three years.Our estimated results for the first four quarters of 2022 are 4.3%, 4.7%, 5.3% and 5.2%, which is consistent with the year-on-year rhythm of this quarter, but at least to some extent reduces the impact of the high base in the first half of 2021. Moreover, the annual economic growth rate under the three-year average is 4.9%, which is closer to the average level of China’s potential growth rate during the 14 th Five-Year Plan period calculated by the People’s Bank of China.

Judging from the economic rhythm depicted by the three-year average growth, the domestic economy was in recession in the first and fourth quarters of 2022 (corresponding to the decline in corporate profits). At this time, the performance of bonds was relatively better than that of equity assets, and the allocation of large-scale assets should be defensive. In the second and third quarters, the domestic economy stabilized and rebounded, and the allocation of large-scale assets should shift to equity assets.

2. Industry is facing the dual impacts of supply constraints and declining demand.

In 2022, global commodity production was limited and the manufacturing supply chain was unstable; The domestic "peak carbon dioxide emissions" goal continues to affect domestic industrial production. Judging from the situation in 2021, even if the export industry and high-tech manufacturing industry maintain rapid growth, it is difficult to resist the economic downturn after the heavy chemical industry production is hit. What’s more, it is difficult for the export industry to repeat the high growth in 2021 in 2022. Therefore, it is expected that the industrial growth rate in 2022 will drop significantly compared with that in 2021.

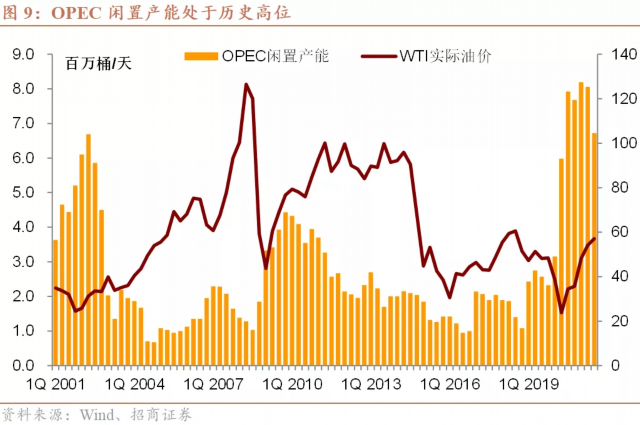

First, the global crude oil production capacity is still limited.Although the current Brent crude oil price has exceeded $80/barrel, OPEC+ countries have no intention of further increasing production. According to EIA estimation, the idle capacity of OPEC countries is as high as 6.72 million barrels per day, which is significantly higher than the pre-epidemic level.

Second, long before the COVID-19 outbreak, the global copper production and capacity had dropped significantly.Among them, the global copper production increased by zero in 2019, only by 0.3% in 2020, and the copper production capacity increased by only 0.3% in 2018 and 0.5% in 2019. Since 2021, the average monthly output of global copper mines has reached 1.729 million tons, which is the highest level in recent years, but the average monthly capacity utilization rate has reached 80.6%, which is less than 5 percentage points from the highest level after the financial crisis. The investment cycle of copper mine is long, which means that the space for monthly expansion of copper mine production in the next few years is less than 10,000 tons.

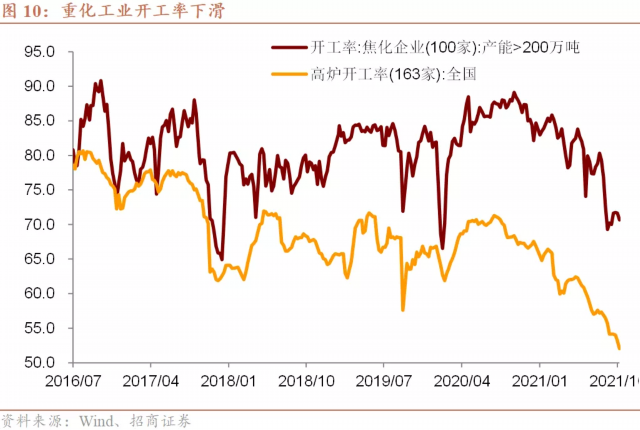

Third, 2021 is the first year of "peak carbon dioxide emissions" goal. The implementation of "sports" policies in some areas has excessively affected the production of some high-energy-consuming industries, caused product shortages and sharp price increases in some areas, and also aggravated the nationwide power cut.At present, the capacity utilization rate of high energy-consuming enterprises has dropped significantly. The capacity utilization rate of coking enterprises has dropped to 71.7%, equivalent to the level in February 2020. The capacity utilization rate of electrolytic aluminum has dropped from 94% at the beginning of the year to around 90%. The national blast furnace operating rate has fallen to 53.2%, which has fallen to the recent historical level. Judging from the added value of different industries, the added value of non-metallic mineral products and steel industry has fallen into a negative growth state year-on-year, and the output of steel, cement and other industries has generally fallen into negative growth. Although the non-ferrous metal industry is supported by the production of new energy metals, the added value of the industry has also fallen to the lowest level since November 2017.

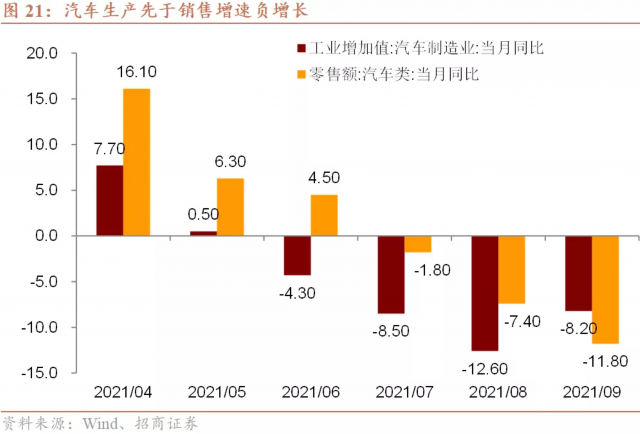

In addition, the instability of the global industrial chain supply chain has also had a significant impact on the production of automobile and other manufacturing industries.In June 2021, after the Malaysian manufacturing PMI fell below the critical value due to the impact of the epidemic, the added value of China’s automobile industry also entered a negative growth state. At present, there are more than 6,000 new cases in Malaysia every day. It will take some time for the supply of automobile chips to fully recover, and the production of domestic automobile industry will still be affected by the lack of chips.

3. The investment structure is further differentiated.

In recent years, investment demand has shown obvious structural differentiation characteristics, including the differentiation of old and new infrastructure investment, the differentiation of high-tech industries and traditional industries. We expect that the investment structure will be further differentiated in 2022 under the background of major changes in the medium and long-term development direction, such as the adjustment and upgrading of the real estate industry, the continuous promotion of peak carbon dioxide emissions and the accelerated pace of common prosperity.

(1) The deterioration of incremental indicators impacts the stability of stock indicators, and the demand for real estate investment shrinks.

In October, 2021, the regulator released the signal to ensure the normal financing demand of real estate, and then the National People’s Congress Standing Committee (NPCSC) authorized the State Council to conduct a real estate tax pilot. The market thought that the possibility of stricter real estate regulation and control policies was obviously reduced, but the impact of previous regulation and control on the real estate market was far from over.

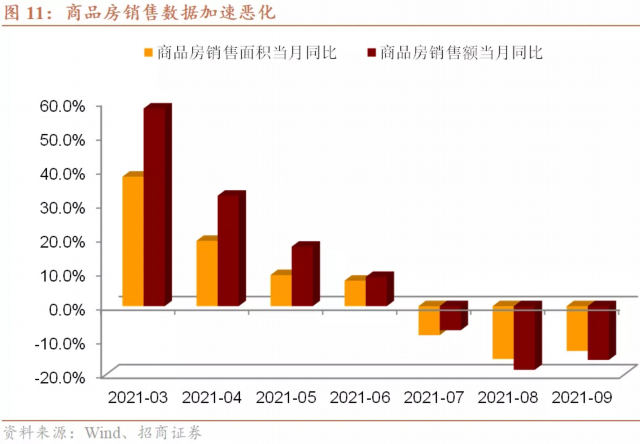

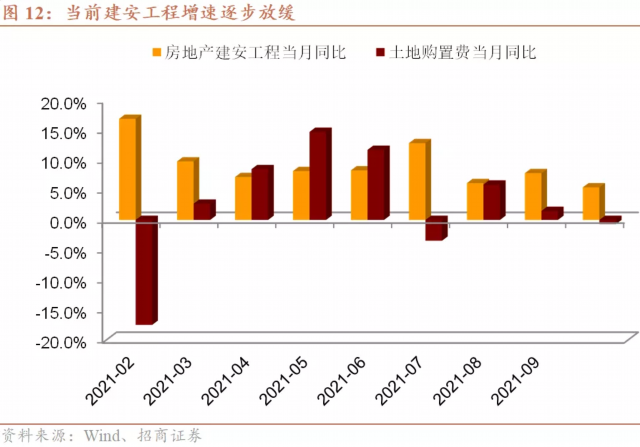

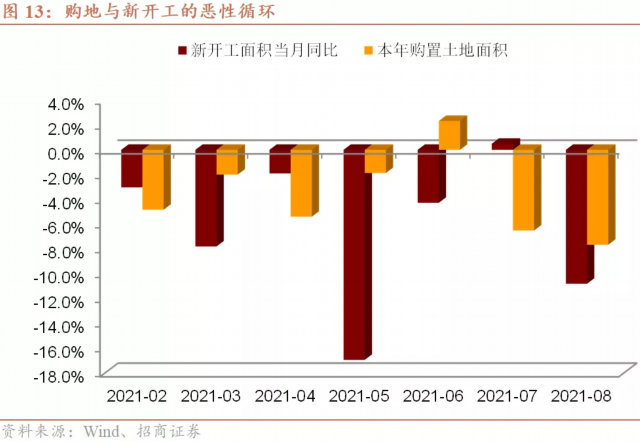

In the first half of 2021, the real estate market benefited from the countercyclical adjustment policy after the epidemic, and the main data related to real estate investment still maintained rapid growth. But in the second half of the year, we observed the rapid deterioration of real estate market data. Since July, the two-year average growth rate of housing construction area and newly started area in the same month has continued to grow negatively, while the two-year average growth rate of commercial housing sales area in the same month has started to grow negatively since August, and the two-year average growth rate of completed housing area and commercial housing sales in the same month has also fallen into a negative growth state in September. The growth rate of the constituent indicators of the completed real estate investment has also slowed down significantly recently. In September, the two-year average growth rate of Jian ‘an project dropped to 5.4% year-on-year, which was 7.4 percentage points slower than that in June. The two-year average growth rate of land acquisition fees in September was negative again, which directly led to the slowdown of the two-year average growth rate of real estate investment in September to 4.0%, which is the lowest level so far this year.

Looking forward to 2022, the main problem of real estate investment lies in the acceleration of housing completion and the serious deterioration of land acquisition data, which may further worsen the newly started area of obvious houses. With the continuous compensation of construction debts, the stabilizing effect of stock data on the growth rate of real estate investment will become increasingly weak.In the first three quarters of 2021, the land acquisition area decreased by 8.5% year-on-year, with an average increase of 5.7% in two years. In fact, since 2019, the land acquisition area has stabilized in a negative growth state. The negative growth of land acquisition area will be translated into the continuous negative growth of newly started housing area in 2022. The continuous negative growth of new construction area and the obvious impact of completion rhythm have been reflected in the housing construction area in 2021. Since 2021, the two-year average growth rate of newly started area-completed area has continued to grow negatively, which means that real estate developers are accelerating the destocking of construction inventory this year. However, this kind of decontamination is unhealthy and unsustainable, and the deterioration of flow data eventually translates into the deterioration of stock data. In September, the two-year average growth rate of new housing construction has dropped to negative growth.

Therefore, for the real estate investment in 2022, on the one hand, the newly started area of houses is likely to maintain a negative growth state, and the support of traffic data for real estate investment continues to decline. On the other hand, with the accelerated completion of real estate, the support of housing construction debts for real estate investment is also declining. The demand for real estate investment will inevitably shrink, and the growth rate of real estate investment will inevitably decline.

(2) The investment in new and old infrastructure is as hot as ice.

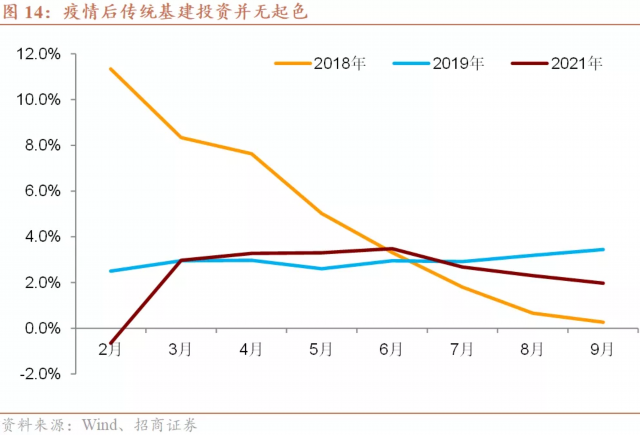

It is estimated that the growth rate of traditional infrastructure investment will remain below 5% in 2022.At present, traditional infrastructure is facing multiple constraints. First, the financial resources of local governments are constrained by preventing risks and declining land revenue; second, factors such as the impact of project quality affect the issuance of special bonds; third, the constraints of peak carbon dioxide emissions’s objectives on traditional infrastructure projects are strengthened; fourth, the demand of cross-cycle adjustment policy framework for smoothing short-term fluctuations is reduced, and the dependence of steady growth policy means on stimulating investment is reduced. Some of these constraints existed before the epidemic, and some were obviously reflected after the epidemic, but in any case, the final result was that the traditional infrastructure investment has been hovering at a low level in the past few years. At present, the two-year average growth rate of infrastructure investment is only 0.4%, of which the two-year average growth rate of investment in water conservancy, environment and public facilities management has been negative for three consecutive months.

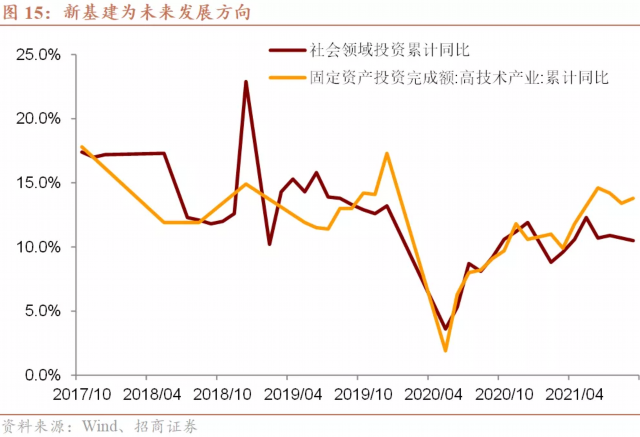

There are two directions in the new infrastructure, both of which are key areas for development at present. First, a new generation of scientific and technological revolution.This is embodied in two indicators: First, investment in information transmission, software and information technology services, with an average growth rate of only 4.0% in the current two years, which is not far from the overall investment, but it is expected that the end of 2021 to the beginning of 2022 will be the key areas for the formation of physical workload.Second, investment in high-tech industries, with an average growth rate of 11.0% in the first two years of 2021, and accelerated to 13.8% in the first three quarters, of which the average growth rate of investment in high-tech manufacturing industries accelerated from 10.7% to 17.1%. Second, investment in social fields related to common prosperity, especially in health and education.In the first three quarters of 2021, investment in social fields increased by an average of 10.5% in two years, 1.7 percentage points faster than at the beginning of the year. Among them, the two-year average growth rate of health investment is 25.7%, and the two-year average growth rate of education investment is 11.5%, both of which are faster than the level at the beginning of the year, and are also greatly related to the overall investment growth rate.

(3) There is a high possibility that manufacturing investment will continue to pick up.

The driving force for manufacturing investment to continue to pick up is mainly reflected in two aspects: First, the growth rate of investment in high-tech manufacturing and strategic emerging industries continues to grow rapidly under the requirements of the new generation of scientific and technological revolution and scientific and technological self-reliance.Since 2015, the investment growth of high-tech manufacturing industry has been sustained and significantly ahead of the manufacturing industry as a whole, and the proportion of high-tech manufacturing investment in all manufacturing investment should also continue to increase, and its influence on the overall manufacturing investment is also increasing day by day. Furthermore, under the goal of peak carbon dioxide emissions, the investment scale of heavy chemical industry is strictly controlled, and the investment structure of manufacturing industry will further change. The prices of resource products have risen sharply in the past year or so, but this year, the investment growth rate of high-tech manufacturing industry is still ahead of energy-consuming industries such as steel, nonferrous metals and non-metallic mineral products.

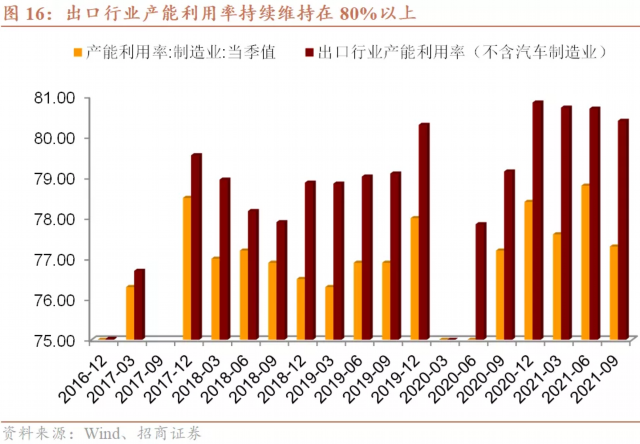

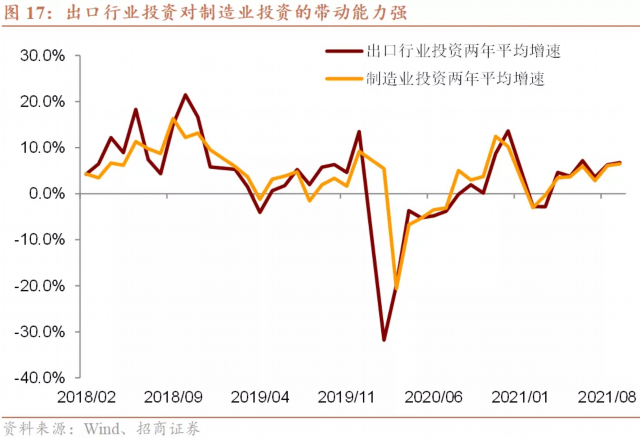

Another driving force for manufacturing investment to continue to pick up comes from the export industry.Although the global economic growth rate has slowed down in 2022, the weak dollar, the spillover of consumer demand and the rising possibility of easing Sino-US economic and trade relations are still conducive to China’s export situation being better than before the epidemic. At present, the capacity utilization rate of China’s export industry excluding automobile manufacturing industry is 80.4%, which has remained above 80% for four consecutive quarters, which is also 3.1 percentage points higher than the overall capacity utilization rate of manufacturing industry in the same period. Since the beginning of this year, the two-year average growth rate of investment in export industry has continued to improve, with the growth rate of -2.8% in the first two months and accelerated to 6.8% in September. Due to the high proportion of investment in export industry in manufacturing industry, the two-year average growth rate of manufacturing investment accelerated from -3.0% to 3.6% in the same period.

We expect that the two logics that manufacturing investment will continue to pick up in 2022 are still valid, and from the credit supply structure since this year, the proportion of medium and long-term loans in manufacturing industry has improved significantly. With the support of funds, policies and the relationship between supply and demand, manufacturing investment will continue the current improvement trend.

4. The improvement direction of consumption is determined, but the degree is uncertain.

In August, 2021, affected by many short-term factors, the social zero month fell to 2.5% year-on-year. In the future, the growth rate of social zero will re-enter the recovery range. However, due to the high uncertainty of income, epidemic situation and other factors, there is also a high uncertainty of the improvement degree of social zero in 2022. The main influencing factors include the following:

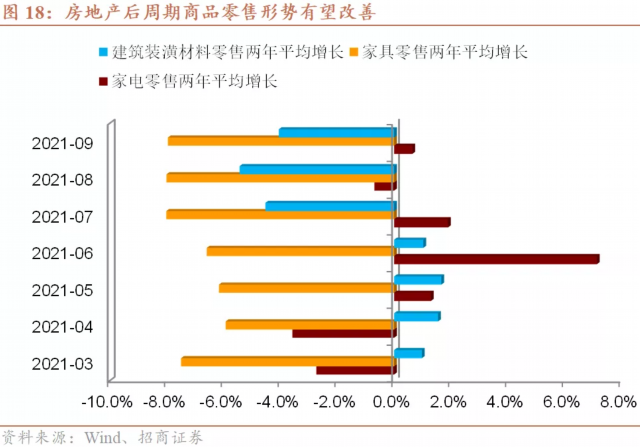

First, after the improvement of real estate credit environment, the recovery of commercial housing sales will drive the improvement of commodity consumption in the post-real estate cycle.Since 2021, the sales of furniture, home appliances and other real estate products have continued to grow negatively, which is one of the main factors that drag down the current zero growth rate. Measured by the average growth in two years, the retail sales of furniture has been negative for seven consecutive years, and it is currently -8.0% year-on-year. The retail sales of home appliances also showed a sluggish performance, with an average monthly growth rate of only 0.6% from March to September, and the retail sales of building and decoration goods continued to grow negatively since July. In the future, with the increase in the amount of mortgage loans, the sales of commercial housing are expected to improve marginally, and related commodities are expected to get out of the continuous downturn.

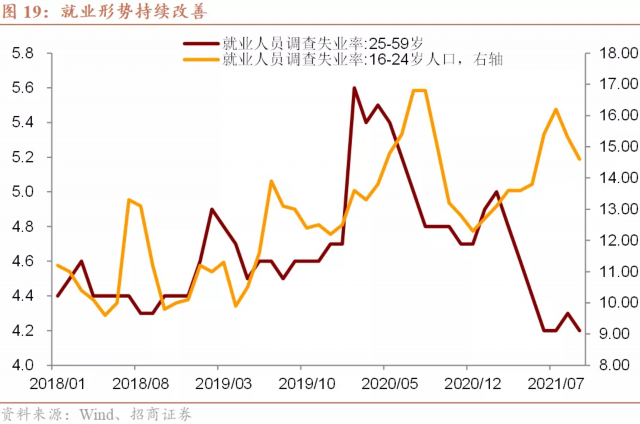

Second, the improvement trend of the employment situation remains unchanged, and the decline in consumption of necessities is only a short-term disturbance.Previously, the unexpected decline in social zero growth rate was closely related to the consumption of necessities. The shrinking demand for necessities comes from the deterioration of employment and income expectations caused by the upgrading of industry governance. However, the latest employment data shows that the anti-seasonal rebound of unemployment rate in mid-2021 may only be a short-term fluctuation. In Q3 of 2021, although the economic situation is not as expected, the urban survey unemployment rate has dropped below 5.0% for the first time since 2019, and the target of newly employed population in cities and towns is nearing completion. The survey unemployment rate of key populations has continued to decline, and the number of migrant workers in rural areas is close to the highest level before the epidemic. Under the framework of cross-cycle adjustment, ensuring employment, people’s livelihood and market players is the primary goal of macro-policy.

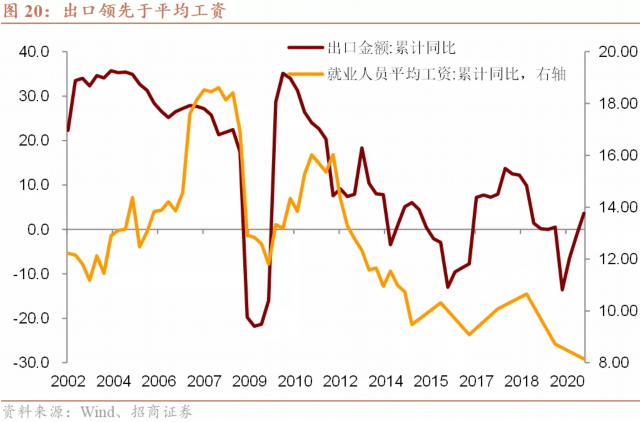

Third, the improvement of exports will increase the average wage level of employed people.Historical data shows that China’s export growth rate will be ahead of the average wage growth rate. From 2002 to 2008, exports continued to achieve a high growth rate of more than 20%, and the average wage growth rate of employed people also rose steadily from about 10% in 2002 to more than 18% in 2007. During the "4 trillion" period, China’s export growth rate rose to over 30% in the second half of 2010. The wage growth rate also returned to 16% in the second half of 2011. After 2012, China’s export growth rate gradually slowed down, with negative growth for two consecutive years from 2015 to 2016, and the wage growth rate also fell to around 9% at the end of 2016. After the outbreak of trade friction between China and the United States, exports approached zero growth in 2019, and the wage growth rate in that year further dropped to 8.7%. We predict that the export growth rate will be close to 30% in 2021, which is significantly higher than that in 2020, which means that the average wage of employed people will also be significantly improved, thus promoting the income growth rate of related industries to rebound.

On the other hand, the consumption situation in 2022 also faces the following negative impacts:

First, the epidemic situation is still an unavoidable problem, which is mainly reflected in catering revenue and automobile retail sales.The former is due to the obvious impact of epidemic prevention and control measures on contact services, while the latter is due to the impact of epidemic on the stability of global supply chain and industrial chain. In recent months, the industrial added value of the automobile manufacturing industry has continued to grow negatively and the decline has been expanding, which has suppressed the demand for automobile consumption on the supply side. According to the data of household survey consumption expenditure, in the first three quarters of 2021, the per capita service consumption expenditure of national residents was 7,781 yuan, up 23.4% year-on-year, and the growth rate was 7.6 percentage points higher than the per capita consumption expenditure. But overall, the recovery degree of service consumption is lower than other consumption. The average service consumption expenditure of the national residents increased by 4.5% in two years, which was 1.2 percentage points lower than that of the residents. The proportion of service consumption expenditure in household consumption expenditure rose by 2.7 percentage points compared with the same period of last year, and it has not yet recovered to the same level in 2019. If the epidemic situation is still not effectively controlled, service consumption and automobile consumption will remain the uncertain factors of the consumption situation in 2022.

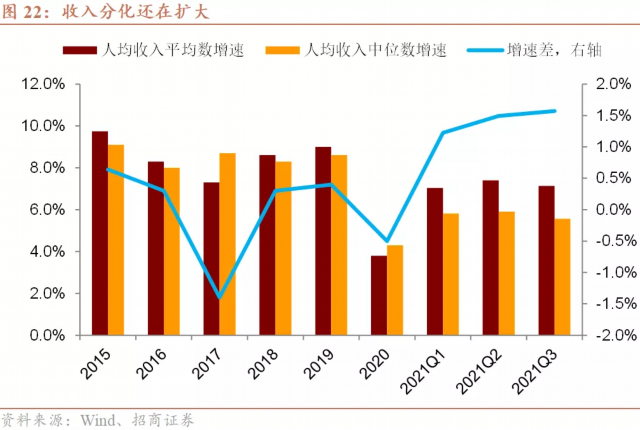

Second, income differentiation intensified after the epidemic.Since the first quarter of 2021, the average growth rate of per capita disposable income has been faster than the median growth rate, and the growth rate difference has been widening — — On a quarter-on-quarter basis, the average growth rate in the first and second quarters was 1 percentage point faster than the median growth rate, and the difference in growth rate in the third quarter widened to 2.4 percentage points. Measured by the two-year average growth, the average growth rate in the third quarter was 1.6 percentage points faster than the median growth rate, while the difference in the first quarter was 1.2 percentage points. From the structural point of view, the growth rate of property income is the highest in all kinds of income, while the marginal consumption tendency of people who hold more assets or wealth is low. If the problem of income differentiation cannot be alleviated, the consumption situation will be affected in 2022.

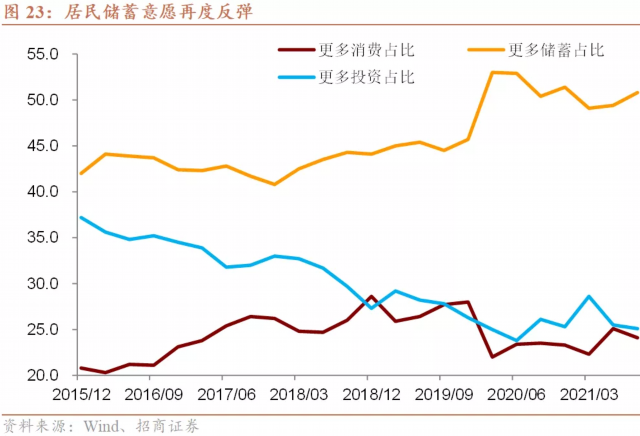

Third, the impact of industry governance is far from over.From the perspective of the average wage level of the industry, the average wage level of the Internet and the financial industry ranked the top two in all industries in 2020. From the perspective of the average wage growth rate, the growth rate of the Internet industry ranked second in 2020, and the average wage level of the agriculture, forestry, animal husbandry and fishery industry ranked first was less than 90,000 yuan, less than 33% of the Internet industry and less than 50% of the financial industry. Any policy has both benefits and costs. Judging from the situation in the third quarter of 2021, although industry governance is helpful to solve the medium and long-term problems of China’s economic development, it will indeed reduce residents’ willingness to consume in the short term and improve the precautionary saving motivation. The People’s Bank of China’s savings questionnaire shows that the proportion of depositors who are willing to spend more in the third quarter of 2021 decreased by 1 percentage point against the seasonal trend, and increased by 0.37 percentage point in the same period in history. From August to September, the new deposits of households reached 2.4 trillion yuan, the highest level in history.

5. The export growth rate has dropped quarter by quarter, and it may still be positive for the whole year.

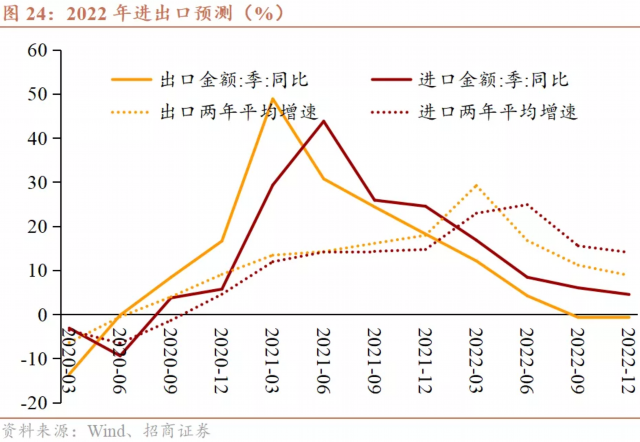

Export forecast:In 2022, although the manufacturing PMI of developed economies may fall back, it is likely to remain in the boom zone, so the demand for restocking and the import of intermediate products will still have some support. However, the immunization progress in emerging economies is relatively backward, and China will still undertake some return orders. Therefore, the annual export growth rate will remain positive. However, due to the base factor, the year-on-year growth rate of the four quarters will weaken quarter by quarter. Therefore, it is predicted that the export growth rate in 2021Q4 will be 18.2%, with an average growth rate of 17.9% in two years. The year-on-year growth rates of exports from Q1 to Q4 in 2022Q1 were 12.1%, 4.2%, -0.7% and -0.7% respectively, and the annual growth rate was 3.2%.

Import forecast:Although the domestic economy is in marginal decline, policies such as special bond issuance and real estate credit have been marginally adjusted, and there is little risk of further economic stall. At the same time, global orders have returned, and domestic processing trade is running smoothly. In terms of commodities, since the gap between supply and demand is difficult to solve in a short time, China will further implement the measures of "ensuring supply and stabilizing prices" to support the import of related commodities. Therefore, it is predicted that the import growth rate in 2021Q4 will be 24.5%, with an average growth rate of 14.7% in two years. From Q1 to Q4 in 2022, the import growth rate was 16.8%, 8.4%, 6.0% and 4.5% respectively, and the annual growth rate was 8.6%.

(1) Exports: Developed economies maintain prosperity, and orders from emerging economies return.

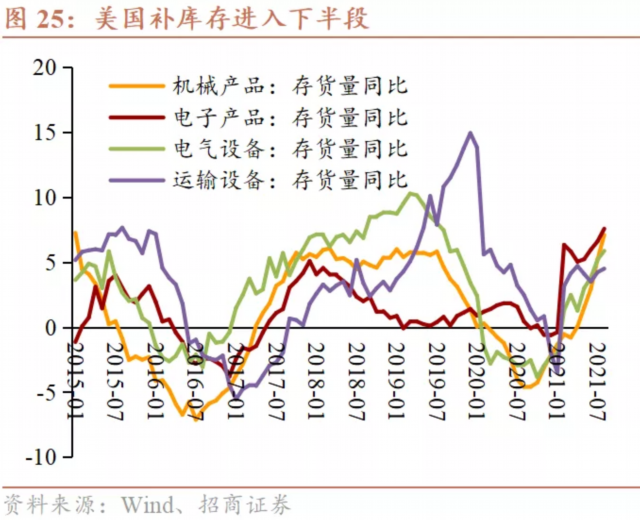

First, although the PMI index of developed economies has declined marginally, it can still maintain the boom zone in 2022.From 2021Q4 to 2022, the developed economies will gradually enter a new stage of "coexistence with the epidemic", the global economy will still maintain a stable recovery stage, the productive demand will remain relatively stable, and the import of intermediate products will maintain a relatively high growth rate. Among them, the United States started the replenishment cycle from 2021Q1, and it is still in the second half of the replenishment cycle, and there is still room for replenishment of machinery, electronics, electrical equipment and transportation equipment.

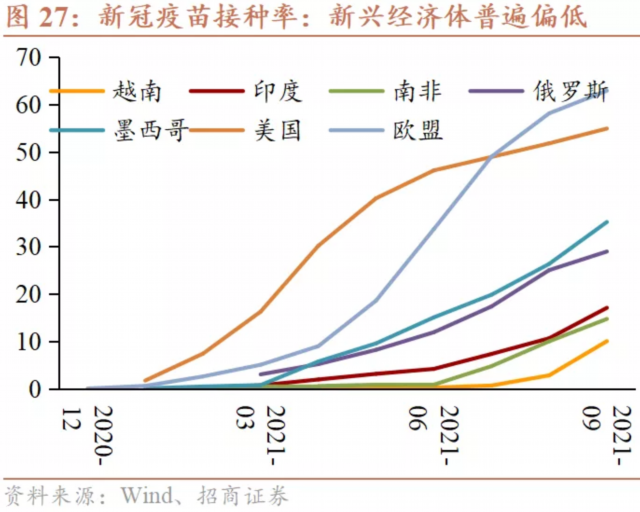

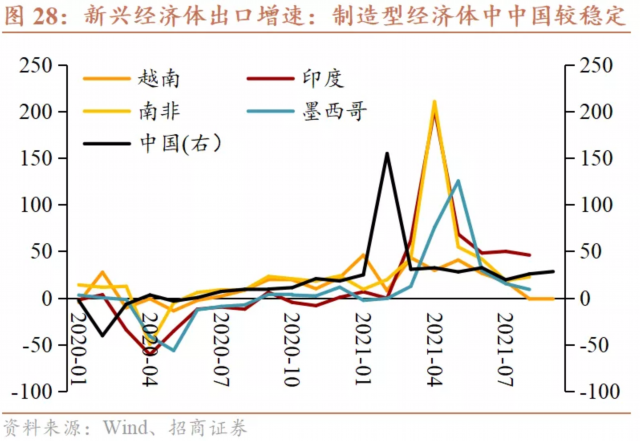

Second, the immunization progress in emerging economies is relatively lagging behind, and China will still undertake some return orders.At present, the global vaccine distribution is extremely uneven, and the vaccination rate gap between developed economies and emerging economies is obvious. Britain, Europe and the United States are relatively high, while Southeast Asia, South Asia and Africa, which rely on imported vaccines, are seriously low. Taking Viet Nam as an example, measures such as blocking factories and restricting the flow of people during the epidemic period triggered the return of orders or production lines to China. The data also shows that since the second half of this year, the export growth rate of India, Mexico, Vietnam and other countries has continued to decline, while China’s exports have maintained a relatively high growth rate.

(2) Import: Processing trade kept smooth, and energy and raw materials grew rapidly.

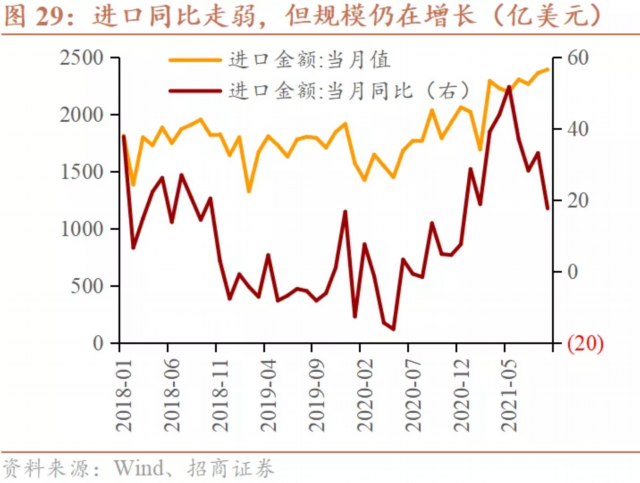

Since the second half of 2021, the domestic prosperity has declined, and the year-on-year growth rate of exports has dropped marginally. However, the growth rate of imports in the next stage still has a supporting force. It is predicted that although imports will decline year-on-year, the annual growth rate will still be 8%, slightly higher than the nominal GDP growth rate.

First, the processing trade remained smooth.The impact of the epidemic on industrial production has been significantly reduced. First, prevention and control measures have greatly reduced the probability of industrial practitioners contacting infected people; Second, practitioners in key units are more likely to get vaccination; Third, the detection efficiency is improved, and infected people are isolated and treated in time. Under this circumstance, the global processing trade will remain relatively smooth, which will also promote China’s imports. The data shows that the year-on-year growth rate of feed processing trade in September has risen to 17.3%.

Second, the import volume of energy, raw materials, chips and agricultural products will continue to grow at a high speed, and their prices will remain relatively high.The above categories are the main imported commodities in China. First of all, in terms of energy, it is difficult to change the situation that crude oil is highly dependent on imports in the short term. In terms of coal, it is necessary to ensure power and heat, give consideration to peak carbon dioxide emissions, and increase imports. Secondly, in industries with high energy consumption such as steel, electrolytic aluminum, cement, flat glass, oil refining, ethylene, synthetic ammonia and calcium carbide, reducing exports, increasing imports or transferring production capacity will help reduce carbon emissions. Thirdly, although the import of chips and agricultural products is affected by Sino-US relations, the actual demand is strong. Finally, since the outbreak of the new crown, there has actually been a global gap between supply and demand for the above-mentioned commodities, so the prices have continued to rise, which has also pushed up the growth of import value.

Macro team of investment promotion: Xie Yaxuan, Luo Yunfeng, Zhang Yiping, Liu Yaxin, Gao Ming and Zhang Qiuyu.